We’ve all heard a lot about insurance. As a general assumption, insurance is something that causes you or the things you have insured to suffer huge financial losses. But there’s more to it than just a cover that you think is capable of causing damage. We will look into it in detail.

What is Insurance?

In technical terms, it is a form of risk management in which the insured entity transfers the cost of potential losses to another entity in exchange for a small monetary compensation. This compensation is calledoverpriced.

In simple terms, it is like paying a lump sum amount to an entity, in order to protect itself from the potential losses that may occur in the future. Thus, when there is a case of some misfortune, the insurer assists you in dealing with the situation.

Also Check: Why insurance is important for you

Why do we need insurance? This question is on everyone’s mind. Do I really need security? Life is full of surprises; Some good, some bad. You need to be prepared for the worst situation that may come your way. It helps you to have a sense of security and peace.

There can be many reasons where you may need help, such as serious illness, natural disaster, unexpected death of loved ones, etc. Being adequately insured in such situations helps significantly in your financial situation. Thus, one should opt for the right type of protection according to one’s needs.

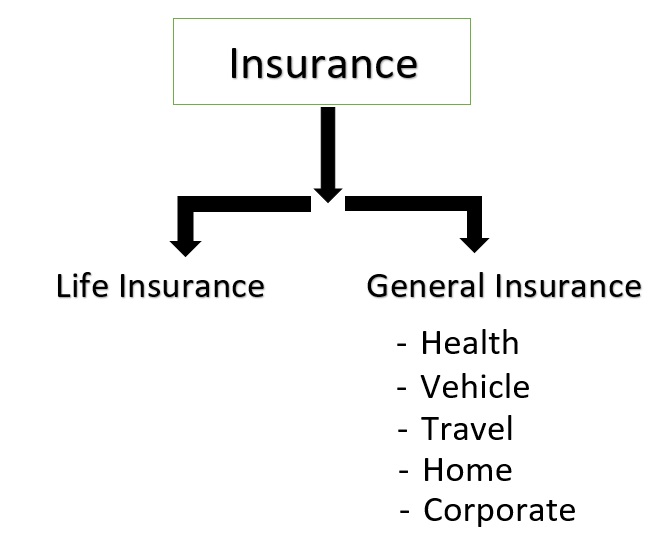

Types of Insurance

1. Life Insurance

Life protection is one of the traditional forms of insurance, designed to protect you and your loved ones from accidental disaster or disaster. It was initially designed to protect theincome of families. But since then, it has evolved only as an alternative to wealth protection from a security measure ortax scheme. The need for life insurance is calculated on various factors such as the number of dependents on an individual, current savings, financial goals, etc.

2. General Insurance

Coverage of any type other than life falls into this category. There are many different types of insurance that cover almost every aspect of your life according to your needs:

a. Health Insurance

It covers your medical and surgical expenses that may arise during your life. Generally, health insurance provides cashless facility in empanelled hospitals.

B. motor insurance

It covers the losses and liabilities associated with a vehicle (two-wheeler or four-wheeler) against different scenarios. It provides protection against vehicle damage and covers for any third party liability stated by law against the owner of the vehicle.

C. travel insurance

This protects you from emergencies or damage that may occur during your trip. It covers you against overlooked medical emergencies, theft or loss of goods, etc.

D. home insurance

It covers the contents of the house and/or inside depending on the scope of the policy. It protects the house from natural and man-made disasters.

E. marine insurance

It covers goods, cargo, etc. from potential loss or damage during transit.

F. commercial insurance

It provides solutions for all sectors of the industry such as construction, automotive, food, electricity, technology, etc. Risk protection needs may vary from person to person but the basic workings of insurance policies remain more or less the same.

How does insurance work?

The most basic principle behind the concept of insurance is ‘risk pooling’. A large number of people are willing to get insurance for a particular loss or damage, and for this, they are willing to pay the desired premium.

This group of people can be called an insurance-pool. Now, the company knows that the number of interested people is huge and it is almost impossible for all of them to need insurance cover at the same time.

Thus, it allows companies to collect funds at regular intervals and also settle the claim when such a situation arises. The most common example of this isvehicle insurance. We all have vehicle insurance, but how many of us have claimed for it? Thus, you pay for and insure for the possibility of damage and you will be paid when a given event occurs.

So when you buy an insurance policy, you pay a regular amount to the company as the premium of the policy. If and when you decide to make a claim, the insurer will pay the loss covered by the policy. Companies use risk data to calculate the likelihood of an event – you’re seeking insurance – happening.

The higher the probability, the higher the premium of the policy. This process is called the process of evaluating the risk to be insured. The company only looks for the actual value of the entity that is insured in accordance with the insurance contract entered into between the parties.

For example, if you have insured your ancestral home for 50 lakhs, the company will only consider the actual value of the house and will not entertain any emotional value for you in the house, because it is almost impossible to put a price on emotions.

There are different terms and conditions for different policies, but the three main general principles remain the same for all types: The cover provided for a property or commodity is for its true value and does not consider any sentiment value.

The probability of the claim should be spread across policyholders so that insurers are able to calculate the probability of risk to determine the premium for the policy. The damage should not be intentional. We have covered the first two points above. The third part is a little more important to understand. Insurance policy is a special type of contract between the insurer and the insured. It is a contract of ‘utmost goodwill’.

This means that there is an unspoken but very important understanding between the insurer and the insured that is generally not present in regular contracts. This understanding includes a duty of full disclosure and not making any false or deliberate claims.

This duty of ‘goodwill’ is one of the reasons why a company may refuse to settle your claim if you have failed to inform them of all the necessary information. And it’s a two-way street. The company has a ‘goodwill’ obligation towards the customer and failing to act on it can cause a lot of trouble to the insurer.

conclusion

Every voicefinancial plan is supported by risk protection. A suitable cover for you is determined by your needs and current financial situation. You should review and re-examine the expenses included in your policy and evaluate its impact on your current financial health.

There are a lot of ifs and but but the basic basic principles of working remain stable on all types of insurance. You should be clear about what type of risk protection you are buying, why you are buying and what is included in the contract.

It is also important for both parties to act in ‘utmost harmony’ so that the entire process of insurance is clear and less troublesome. And as is the case with every financial product, you should be well aware of that product and informed about the product you are buying and get good advice from yourself. Financial Advisor.